What I Changed My Mind About in 17 Years as an Investor

Sometimes the smartest move you can make is choosing the simplest path.

I started investing in 2009.

Back then, I was exposed to Warren Buffett’s way of investing. The Oracle of Omaha, as he is fondly called, amassed a portfolio that has grown at an annualised rate of close to 20% over the long term.

It was all about picking strong companies at the right price, holding them for the long term, and letting compounding do the heavy lifting.

Similarly, my approach to investing was straightforward: Aim for 15% annualised returns, compound that over a couple of decades, and hit a couple of million dollars. That was the plan.

The problem?

I never really questioned why it had to be X million dollars. It was just a big, round number that felt nice to have.

And chasing that return made me take on more risk than I needed to. Sometimes, overweighting positions more than necessary and spending a lot of mental energy trying to squeeze out every extra percentage point. Luckily, I never went down the path of speculative stocks or assets such as meme stocks or crypto.

Also, luckily, I had emergency funds set aside, and I had adequate insurance in place.

Then Life Happened

Over the years, a lot has changed. I got married. I switched industries. And then the biggest shift of all? Having kids.

Suddenly, the time I used to spend poring over annual reports and monitoring my portfolio started competing with Saturday mornings at the playground and bedtime stories.

I realised I didn’t have the bandwidth to actively manage a stock portfolio comprising over 15 companies anymore.

I had known about passive investing since day one, but I always brushed it aside because picking individual stocks was more fun and intellectually stimulating. There’s a certain thrill in discovering a small company before everyone else catches on.

Index funds just felt… boring. But the big push came from a simple shift in mindset.

A Simple, Yet Powerful Reframing

I came across the concept of the Philosophy of Enough or Sufficiency, and it completely reframed how I thought about money.

The idea is simple but powerful.

Instead of asking “How do I maximise my returns?”, I started to ask “What returns are enough to reach my goals, without taking on excessive risk?”

That one question changed everything for me.

When I sat down and actually mapped out what my family needed, I realised I didn’t need to chase 15% returns. I needed a reliable way of investing.

So, I made the switch.

Early 2024, I moved fully into passive investing: broad-based, low-cost index funds and exchange-traded funds (ETFs).

Simple. Boring. But incredibly freeing.

There’s a Reason for Everything

Those early years of picking individual stocks, however, weren’t wasted.

Starting early and investing in fundamentally-strong companies gave my portfolio a meaningful head start. The compounding from those years is something I’m grateful for.

But if someone asked me today how they should invest, especially a busy parent juggling work, kids, and life, I wouldn’t encourage them to start the way I did. Unless they have the interest to analyse companies and the time to do so.

I would rather say the following:

1. Start with your why.

2. Figure out what “enough” looks like for you and your family.

3. Then find the most reliable way to get there. For most people, that’s low-cost index funds.

Spend your mental energy on the things that actually bring you joy, such as watching your kids grow up, instead of focusing on the earnings call during your kid’s soccer practice.

Various Data Back Passive Investing

Even though Warren Buffett runs his own stock portfolio, he has repeatedly said that the vast majority of investors would be better off indexing. For instance, in his 1993 letter, he wrote:

“By periodically investing in an index fund, the know- nothing investor can actually out-perform most investment professionals.”

The evidence for passive investing is also pretty overwhelming.

From 2008 to 2017, Buffett bet that a simple S&P 500 index fund would beat a curated basket of hedge funds. The index fund returned 7.1% annualised. The basket of hedge funds returned an average of only 2.2% per annum, net of all fees. It wasn’t even close, with the winnings going to charity.

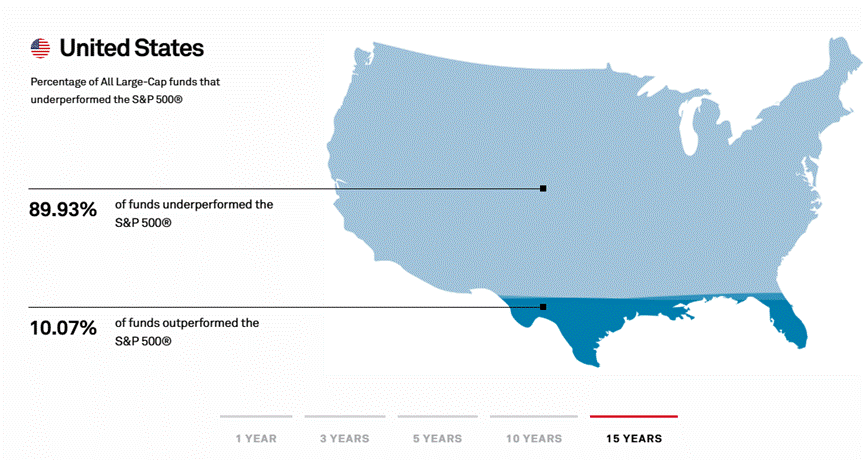

Another data from S&P Dow Jones Indices (SPIVA) shows that 90% of actively managed funds underperform their benchmarks over long horizons.

People who do this full-time – with teams of analysts and access to resources most of us don’t have – would have failed to beat a simple, low-cost index fund.

If the professionals struggle to outperform consistently, it puts things into perspective for the rest of us, especially if we’re doing this on the side while managing careers and raising families.

The beauty of index investing isn’t just the returns. It’s the mental freedom.

Instead of spending your limited bandwidth analysing earnings reports and second-guessing your picks, you can channel that energy into what actually matters to you.

For me, that’s being present with my kids. For you, it might be something similar or entirely different.

But the principle is the same: spend your mind space on what makes you happy.

Everyone’s Journey Is Different

I’m not here to tell you that passive investing is the only way.

What I’m saying is that after 17 years, the one thing I changed my mind about was this: more returns don’t always mean a better life for my family. Sometimes, enough is the most powerful number in investing.

I hope sharing my perspective helps someone out there who’s in a similar place, maybe at a crossroads between the thrill of stock picking and the pull of wanting to simplify.

Quick Action Steps for Busy Parents

If this resonated with you, here are a few things you can do this week:

1. Define your “why.” Before you look at any stock or asset class, write down what you’re actually investing for. Your kids’ education? Early retirement? The freedom to work less? A clear purpose changes every decision that follows.

2. Calculate your “enough” number. Work backwards from your goal. How much do you actually need, and by when? You might find that a steady 7% to 8% from index funds gets you there without the stress of chasing 15%.

3. Protect what you have before growing it. Make sure your emergency fund, insurance, and basic financial safety nets are in place. No investment strategy matters if an unexpected event wipes out your foundation.

4. Start with low-cost index funds. You don’t need to overhaul your entire portfolio overnight. A broad-based global is a solid starting point. Keep costs low by looking for expense ratios under 0.20%.

5. Automate your contributions. Set up a regular investment plan so money goes into your index fund automatically each month. This removes the temptation to time the market and frees up your mental energy for everything else.

Investing doesn’t have to be complicated to be effective.

Sometimes, the smartest move a busy parent can make is choosing the simplest path and spending the time you save on the moments that truly compound.

The Compounding Dad’s 3 Rules:

Know your enough

Spend less than what you earn

Invest the difference in a simple manner

Thanks for your comments, IGP Paradox. Passive or active, market crashes are inevitable. My "mental game" for either way of investing would be to always focus on the long term, fundamentals of a company (if stock picking), and staying the course through the volatility.

As a previous active investor, I also didn't 'select' my way out of volatility by buying defensive stocks. I bought more of the same stocks if they were still fundamentally strong. For passive investing, it makes my decision making much easier since I just buy that index fund (as opposed to choosing which company to average down on). Thanks for your question. Made me reflect. I've written about this part in a previous article here: https://www.thecompoundingdad.com/p/providend-philosophy-of-sufficiency

Great read